{kind=link}

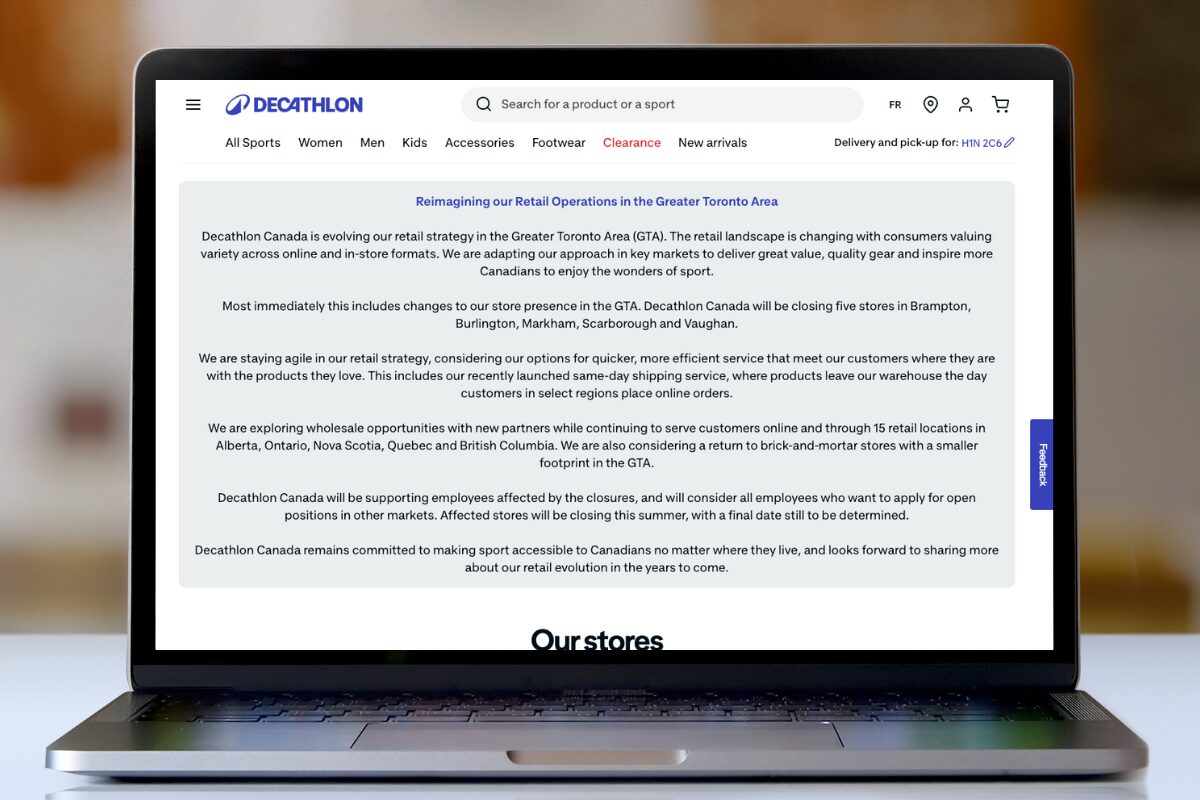

Decathlon Canada will close five Greater Toronto Area stores this summer, ending the French sporting goods retailer’s presence in Brampton, Burlington, Markham, Scarborough, and Vaughan. The closures represent a strategic retreat from Canada’s largest retail market but create immediate opportunities for retailers positioned to capitalize on evolving consumer preferences toward experiential shopping.

The world’s largest sporting goods retailer cited “evolving retail strategy” as the reason for the GTA pullback, with plans to explore smaller footprint concepts and wholesale partnerships. The company will maintain 15 locations across Alberta, Ontario, Nova Scotia, Quebec, and British Columbia, with only one remaining Ontario store in Ottawa.

Market Dynamics Drive Strategic Shift

Lisa Hutcheson, Managing Partner at J.C. Williams Group, attributes the exit to broader market challenges facing international retailers in Canada. “It seems to highlight the challenges of operating in Canada’s mid-tier sporting goods market,” Hutcheson explains. “There seems to be the extremes between value (e.g. Canadian Tire) and premium brands. Like other foreign entrants we have witnessed struggling in the Canadian market, they seem to lack understanding the market.”

The closure aligns with industry-wide transformation patterns. “Canadian retail is leaning to more localized strategies,” Hutcheson notes. “We are also seeing smaller, more agile store formats while at the same time, more experience driven retail with specialized assortments.”

Strong Market Fundamentals Support Growth

Despite Decathlon’s departure, Canadian sporting goods market indicators remain robust. Industry retail sales have increased by nearly 15 billion Canadian dollars since 2017, while the broader North American sporting goods market projects growth from USD 176.9 billion in 2025 to USD 410.3 billion by 2035, representing an 8.5% compound annual growth rate.

Canada’s sporting goods industry maintained 5.4% compound annual growth between 2019 and 2024, reaching $11.5 billion in market size for 2025. McKinsey’s 2025 sporting goods industry report indicates 44% of industry executives express optimism about 2025 prospects, citing successful expansion strategies by newer brands through targeted growth approaches and innovative value propositions.

Prime Real Estate Opportunities Emerge

The GTA retail sector recorded strong investment performance in Q1 2025, with $935 million in transaction volume representing 59% year-over-year growth. Investors demonstrated particular interest in food-anchored retail properties and shopping centers offering redevelopment potential, according to Altus Group market data.

Hutcheson emphasizes strategic considerations for potential occupants of the vacated spaces: “It will depend on how well the next occupant can align their offer to meet the trade area needs and wants as well as understanding the traffic patterns of the property. Omnichannel integration will also need to be present as next generation consumers are expecting a seamless experience across all channels.”

Experiential Retail Becomes Market Imperative

Consumer behavior data reveals shifting purchasing patterns favoring experiential retail formats. Traditional online search (35%), in-store experiences (33%), and peer recommendations (31%) remain primary factors influencing sporting goods purchases across demographic segments.

“Experiential retail is becoming essential in this category as consumers increasingly seek engaging shopping experiences rather than purely transactional ones,” Hutcheson states. “Consumers are expecting spaces where they can test equipment, try on apparel, or experience products in action, such as running tracks, climbing walls, or VR-enhanced simulations.”

Demographic analysis shows over 50% of Gen Z and Millennials identify social media as a product discovery driver, compared to 25% of Gen X and 8% of Baby Boomers. These younger consumers also demonstrate higher acceptance of secondhand purchases, with over 50% willing to buy pre-owned sporting goods versus 18% of Baby Boomers.

Hutcheson identifies specific experiential trends: “Personalization services is also adding to the service offer—like gait analysis for running shoes. Fitness club/events, pop-up classes, are very popular right now, especially with Gen Z and Millennials that are trading late-night clubbing with these sport focused clubs and experiences—fostering a sense of belonging and loyalty.”

Independent Retailers Gain Competitive Advantage

Market analysis indicates independent sporting goods retailers possess structural advantages over large international chains. Source for Sports operates 130+ locally owned stores across Canada, demonstrating successful community-focused retail models through customized product selection and localized service offerings.

Hutcheson outlines key independent retailer advantages: “Independent sporting goods retailers have advantages over the large international chains such as: Localization and tailoring their product mix to the specific needs of their local community, offering niche products or services that resonate with regional sports trends and preferences.”

Operational agility provides additional competitive benefits. “Local retailers often excel at building personal connections with their customers, providing personalized recommendations and fostering loyalty through exceptional service,” she explains. “Indie retailers can often quickly adapt to market changes, introduce new product lines, or pivot their strategies without the bureaucratic constraints faced by large chains.”

The contrast with standardized retail approaches becomes evident in customer preferences. “Large international chains like Decathlon often rely on standardized global strategies, which can fail to resonate with Canadian consumers who value local expertise and authenticity,” Hutcheson notes.

Technology Integration Drives Innovation

Advanced sporting goods technology continues expanding market opportunities. Demand increases for smart, connected equipment featuring IoT capabilities, including fitness trackers and sensor-embedded gear that enhance athletic performance and lifestyle fitness applications.

Forward-thinking retailers integrate sophisticated services including bike power meter installation and data analysis, running store VO2 max testing, and golf retailer launch monitors with custom fitting software. These specialized services require expertise, relationship-building, and trust—capabilities that differentiate local retailers from big-box formats.

Strategic Success Framework

Hutcheson provides three critical strategic considerations for retailers evaluating former Decathlon locations:

Space optimization represents the primary consideration: “Evaluate whether the large-format space works for their model. Consider hybrid models that integrate retail with experiential zones, such as fitness studios, product demo areas, or community event spaces.”

Market analysis ensures appropriate positioning: “Conduct a detailed market analysis to understand local demographics, sports preferences, and spending habits. Tailor the product mix and services to meet the specific needs of the surrounding community, whether it’s hockey equipment in suburban areas or yoga gear in urban centers.”

Omnichannel integration provides competitive differentiation: “Ensure there is an omnichannel strategy that seamlessly connects in-store and online experiences. Use the physical location to enhance brand engagement through click-and-collect options, personalized consultations, or exclusive in-store experiences that complement the convenience of e-commerce.”

Future Market Outlook

Specialty retailers position themselves as community hubs through local sports sponsorships, workshops, and training programs. These partnership strategies with local athletes and organizations increase brand awareness while building customer loyalty—approaches that large-format international retailers struggle to replicate effectively.

The sustainable retail segment presents additional growth opportunities, with younger demographics showing increased interest in trade-in programs, refurbishment services, and consignment partnerships that extend product lifecycles.

Decathlon’s GTA market exit signals retail evolution rather than industry decline. The departing retailer’s shift toward wholesale partnerships and smaller footprint concepts acknowledges changing consumer preferences while creating opportunities for retailers equipped to deliver localized expertise and experiential shopping environments.

For sporting goods retailers prepared to invest in community engagement, technological integration, and experiential retail formats, Decathlon’s departure represents a strategic opening in one of Canada’s most valuable retail markets.

Dustin Fuhs is the founder and Editor-in-Chief of 6ix Retail, Toronto’s premier source for retail and hospitality industry news. As the former Editor-in-Chief of Retail Insider, Canada’s most-read retail trade publication, Dustin brings over two decades of expertise spanning retail, marketing, entertainment and hospitality sectors. His experience includes roles with industry giants such as The Walt Disney Company, The Hockey Hall of Fame, The Canadian Opera Company, Starbucks Canada and Blockbuster.

Recognized as a RETHINK Retail Top Retail Expert in 2024, 2025 and 2026, Dustin delivers insider perspectives on Toronto’s evolving retail landscape, from emerging brands to established players reshaping the city’s commercial districts.